$0.00

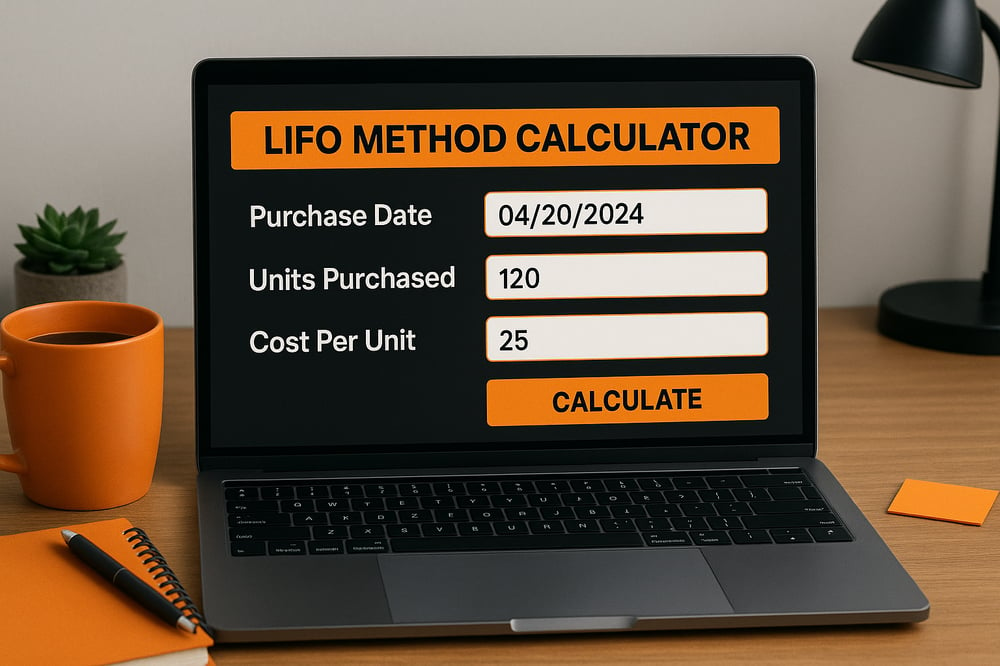

LIFO Inventory Calculator

Purchase Date

Units Purchased

Cost per Unit

Total

Results:

Total COGS: $0.00

Ending Inventory: 0 units

Looking to simplify and optimize your inventory valuation process? Our LIFO Method Calculator is designed to provide accurate assessments of inventory costs using the Last-In, First-Out method.

Whether you’re managing inventory for a thriving e-commerce business or a large-scale operation, this tool empowers you to calculate the Cost of Goods Sold (COGS) and ending inventory values with ease, helping you make informed financial decisions.

Start calculating now to gain clarity, streamline your accounting, and take control of your inventory management strategy!

Understanding Each Component of the LIFO Inventory Calculator + Examples

Here’s a detailed breakdown of each component in the LIFO (Last-In, First-Out) Inventory Calculator, complete with examples and scenarios to help you understand how each element affects your inventory valuation and cost calculations.

1. Purchase Entries

This multi-entry section allows you to input your inventory purchases chronologically, tracking both quantity and cost variations over time.

Examples:

- Seasonal Retailer

- January Purchase: 1,000 units at $10/unit

- March Purchase: 1,500 units at $12/unit

- June Purchase: 2,000 units at $15/unit

- Total Inventory: 4,500 units

- Layered Cost Structure: $38,500

- Electronics Store

- Q1 Purchase: 500 units at $100/unit

- Q2 Purchase: 750 units at $120/unit

- Q3 Purchase: 1,000 units at $95/unit

- Total Inventory: 2,250 units

- Layered Cost Structure: $267,500

Why It Matters: Purchase entries create your inventory layers, which are fundamental to LIFO calculations. More recent purchases are considered sold first, potentially leading to higher COGS in inflationary markets.

2. Date Selection

Each purchase entry includes a date field to track when inventory was acquired.

Examples:

- Manufacturing Company

- Layer 1: March 1 – Raw Materials

- Layer 2: March 15 – Additional Stock

- Layer 3: March 30 – End-of-Month Purchase

- Wholesale Distributor

- Layer 1: Q1 Bulk Purchase

- Layer 2: Mid-Year Restock

- Layer 3: Peak Season Inventory

Why It Matters: Dates help track inventory aging and ensure proper LIFO order application, especially important for businesses with frequent price fluctuations.

3. Units and Cost Fields

These fields capture the quantity and per-unit cost of each inventory purchase.

Examples:

- Food Distributor

- January: 5,000 units at $2.00/unit

- February: 4,000 units at $2.25/unit

- March: 6,000 units at $2.50/unit

- Apparel Retailer

- Spring Collection: 2,000 pieces at $15/piece

- Summer Collection: 3,000 pieces at $18/piece

- Fall Collection: 2,500 pieces at $20/piece

Why It Matters: Accurate unit and cost tracking ensures proper inventory valuation and helps identify cost trends over time.

4. Total Cost Calculation

Automatically calculates the total cost for each inventory layer.

Examples:

- Auto Parts Supplier

- Layer 1: 1,000 units × $50 = $50,000

- Layer 2: 1,500 units × $55 = $82,500

- Layer 3: 2,000 units × $60 = $120,000

- Building Materials

- Layer 1: 500 units × $100 = $50,000

- Layer 2: 750 units × $110 = $82,500

- Layer 3: 1,000 units × $115 = $115,000

Why It Matters: Layer totals help track invested capital and provide quick insights into inventory value distribution.

5. Units to Sell Input

This field determines how many units will be calculated using the LIFO method.

Examples:

- Tech Retailer Scenarios

- Small Sale: 100 units (uses most recent layer)

- Medium Sale: 500 units (spans multiple layers)

- Large Sale: 1,000 units (requires multiple layer calculation)

- Manufacturing Scenarios

- Regular Production: 1,000 units

- Peak Production: 2,500 units

- Special Order: 5,000 units

Why It Matters: The number of units to sell determines which layers will be used in COGS calculation and how the LIFO method is applied.

Results Breakdown

Provides detailed calculation results including COGS and inventory analysis.

Example Calculations:

- Scenario 1: Rising Costs

- Initial Inventory:

- Layer 1 (Oldest): 1,000 units at $10 = $10,000

- Layer 2: 1,000 units at $12 = $12,000

- Layer 3 (Newest): 1,000 units at $15 = $15,000

- Selling 1,500 units (LIFO Method):

- Use Layer 3: 1,000 units × $15 = $15,000

- Use Layer 2: 500 units × $12 = $6,000

- Total COGS: $21,000

- Initial Inventory:

- Scenario 2: Mixed Cost Pattern

- Initial Inventory:

- Layer 1 (Oldest): 2,000 units at $20 = $40,000

- Layer 2: 1,500 units at $18 = $27,000

- Layer 3 (Newest): 2,500 units at $22 = $55,000

- Selling 3,000 units (LIFO Method):

- Use Layer 3: 2,500 units × $22 = $55,000

- Use Layer 2: 500 units × $18 = $9,000

- Total COGS: $64,000

- Initial Inventory:

By understanding these components, you can confidently use the LIFO Inventory Calculator to streamline your inventory valuation process, optimize financial reporting, and make informed decisions for your business.

Pros and Cons of Using LIFO for Inventory Accounting: Is It Right for Your Business?

The Last-In, First-Out (LIFO) inventory valuation method has its unique strengths and limitations. Understanding these pros and cons is essential to determine whether LIFO is the right fit for your business. Here’s a breakdown of the key advantages and disadvantages:

Advantages of LIFO Accounting

Tax Benefits During Inflation:

When prices rise, LIFO assumes the most recent (and often higher-priced) inventory is sold first. This results in a higher Cost of Goods Sold (COGS), which reduces taxable income.

Example: If inventory costs increase from $10 to $15 per unit during inflation, LIFO will use the $15 cost first, lowering profits on paper and consequently reducing tax liability.

Accurate Profit Reflection in Inflationary Times:

LIFO provides a more realistic view of current expenses by matching the latest inventory costs to current revenues. This helps businesses avoid overstating profits during inflation.

Cash Flow Advantages:

Lower taxable income translates to improved cash flow, which can be reinvested in growth, paying down debt, or operational improvements.

Disadvantages of LIFO Accounting

Lower Net Income:

While LIFO reduces taxable income, it also shows lower net income on financial statements. This can make your business appear less profitable to stakeholders and investors.

Compliance Restrictions:

LIFO is not allowed under International Financial Reporting Standards (IFRS), which means businesses operating globally might face challenges in consolidating their financials.

Complex Inventory Management:

Implementing and maintaining LIFO can be cumbersome, as it requires meticulous tracking of inventory layers and purchase costs over time.

Potentially Distorted Balance Sheets:

LIFO may undervalue ending inventory during inflation since older, lower-cost inventory remains on the books. This can lead to an inaccurate representation of your company’s assets.

Common Use Cases for LIFO Accounting: When Does It Make Sense?

LIFO accounting is particularly advantageous in specific industries and scenarios. Here are some common situations where LIFO shines:

Inflationary Markets

Why It’s Beneficial: During inflation, LIFO reduces taxable income by assigning higher costs to COGS. This method is especially valuable in industries experiencing frequent price hikes, such as:

- Construction: Rising material costs like steel and cement.

- Energy: Volatile fuel and oil prices.

Retail Industry

Example: A clothing retailer with seasonal inventory turnover can benefit from LIFO when costs rise. By valuing newer, more expensive inventory as sold, they reduce taxable income while keeping older inventory on hand.

Why It Works: Retailers frequently face fluctuating costs for materials, making LIFO an effective tool for matching revenue with expenses.

Automotive Sector

Example: Auto manufacturers and dealers often experience price changes in raw materials and components. LIFO ensures these businesses account for these changes accurately.

Electronics and Technology

Why It’s Ideal: The fast-paced nature of the electronics industry results in constant updates and cost changes. Using LIFO ensures businesses account for the latest (often pricier) inventory first.

Manufacturing Companies

Scenario: A factory producing goods from materials like metals or chemicals can use LIFO to match higher costs with revenue, especially during peak production cycles.

Regulatory Considerations for LIFO Accounting: What You Need to Know

LIFO isn’t universally accepted, and its regulatory environment varies significantly. Here’s what you need to know:

Where LIFO Is Allowed

U.S. GAAP (Generally Accepted Accounting Principles):

LIFO is permissible under GAAP, making it a popular choice for businesses operating primarily in the United States.

Where LIFO Is Prohibited

International Financial Reporting Standards (IFRS):

LIFO is not accepted under IFRS, which is followed by most countries outside the U.S. Companies operating globally must adopt other inventory valuation methods, like FIFO or Weighted Average Cost, to remain compliant.

Challenges for Multinational Companies

Dual Compliance: Businesses with operations in both LIFO-allowing and LIFO-prohibiting regions may face complexities in consolidating financial statements.

Example: A U.S.-based company using LIFO might need to adjust its reporting to FIFO for its European operations under IFRS.

Tax Implications

LIFO Conformity Rule: In the U.S., if you use LIFO for tax purposes, you must also use it for financial reporting. This ensures consistency but can impact how your financial health is perceived by investors.

Record-Keeping Requirements

LIFO requires detailed tracking of inventory layers, which can be resource-intensive. Compliance demands that businesses maintain accurate records of purchase dates, quantities, and costs.

Leverage LIFO for Smarter Inventory Decisions

The LIFO Method Calculator is your go-to tool for simplifying inventory valuation, calculating Cost of Goods Sold (COGS), and determining ending inventory with precision.

By understanding LIFO’s benefits, use cases, and compliance requirements, you can align your inventory accounting with your business goals. Whether you’re navigating inflationary markets or managing high-turnover industries, this calculator provides the clarity you need to make informed financial decisions.

With actionable insights and accurate results, the LIFO method empowers you to streamline your accounting process, optimize cash flow, and stay ahead of inventory challenges.